Payments, identity checks and withdrawals in Great Britain gambling

Start with the regulated-market baseline

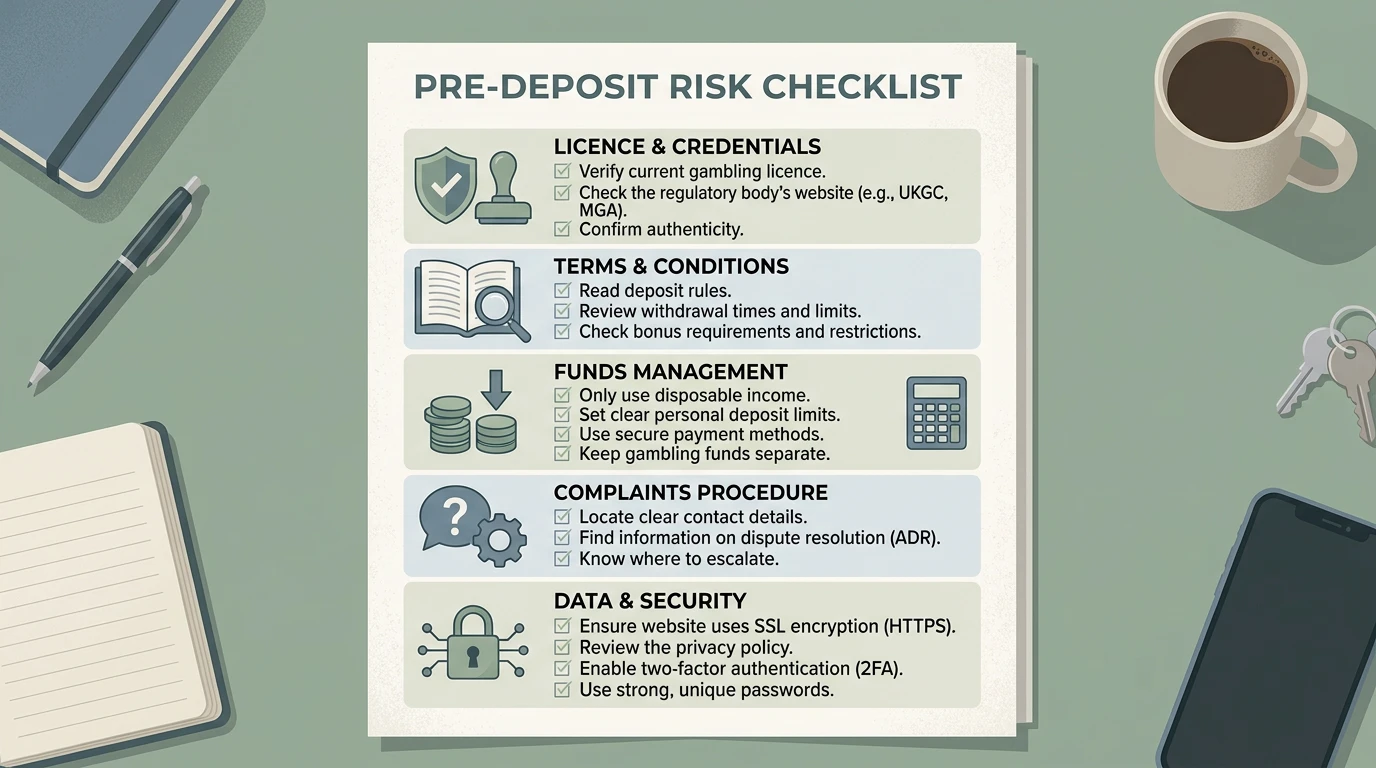

In the Great Britain regulated market, gambling businesses licensed by the Gambling Commission must not accept credit-card gambling payments. The same restriction applies where an e-wallet is funded by a credit card for gambling. That baseline is useful because it stops a common misunderstanding: a payment restriction is not necessarily a technical fault, and it should not be treated as something to work around.

For a reader comparing sites outside the usual GAMSTOP boundary, this matters because payment claims can be used to make a site look easier or more convenient. “Easy deposit”, “no card checks” or “instant cashout” wording should never replace a licence check, clear terms and an understanding of what happens when the business asks for identity documents. The more a site presents protection checks as optional or irritating, the more carefully the claim should be read.

Online gambling businesses licensed in Great Britain must verify age and identity before gambling. Official guidance describes identity checks as including details such as name, address and date of birth. That does not mean every customer journey feels identical, but it does mean a confident “no documents ever” message should be treated with caution. A site can request documents later for fraud, withdrawal, account or source-of-funds reasons, and a user who deposits without reading those conditions may discover the friction only when trying to withdraw.

What identity checks are trying to do

Identity checks are often discussed as if they only protect the operator. In a regulated setting they also support age controls, account ownership checks and the prevention of misuse. A request for name, address or date of birth is not automatically a sign of wrongdoing; it can be part of the normal gatekeeping that should happen before gambling. The problem is lack of clarity: if a website hides when checks happen, what documents may be requested, or what happens to a withdrawal during a review, the customer is left guessing.

Before depositing, read the terms that explain verification, account ownership, withdrawal review, bonus restrictions and document requirements. The useful question is not “How can this be avoided?” The useful question is “Is the process clear enough that I would still be comfortable if a withdrawal were paused for a document check?” If the answer is no, the risk belongs to the customer, not to the slogan on the homepage.

Financial vulnerability checks also sit in this area. The Gambling Commission has described official thresholds for checks in the regulated market, and the purpose is protective. A public guide should not explain how to avoid those checks. It can explain that checks are not the same as a personal judgement, and that a customer should be wary of any site that presents the absence of checks as a benefit without also showing a strong, verifiable protection framework.

Financial limits are not window dressing

Remote gambling systems regulated in Great Britain must provide customer financial-limit facilities. Deposit-limit rules are also changing from 30 June 2026 to make the way limits are offered and described clearer for consumers. The practical point is simple: limits should be treated as part of the product, not as an afterthought hidden in account settings.

A responsible review of any gambling site should ask where limits are set, whether they are easy to find, whether the wording is clear, and whether cooling-off or increase rules are explained. The answer may affect how risky the account feels in real use. If limits are hard to locate, described vaguely, or presented as a feature that can be removed with little friction, that weakens the customer’s control.

Bank gambling blocks are another protective tool. Some banks allow customers to block transactions categorised as gambling. If a bank block is active, the safest interpretation is that the block is there for a reason. A guide should not give routes around it. If the block was set during a period of concern, trying to defeat it can turn a financial tool into a warning that help or a pause may be needed.

Decision path for common payment and withdrawal situations

| Situation | What it may mean | Safer next step |

|---|---|---|

| Before depositing | The important facts are still within your control: licence status, terms, identity requirements, withdrawal rules and limits. | Check the Gambling Commission register first if the site claims to serve Great Britain, then read payment and withdrawal terms before entering money details. |

| Asked for ID | Age and identity checks can be normal in a regulated setting, but vague or shifting requests can also create frustration. | Pause new deposits, read the verification terms, keep copies of messages and do not send documents through channels that look insecure. |

| Payment blocked | A credit-card restriction, e-wallet funding issue or bank gambling block may be a protective control rather than an error. | Do not look for a workaround. Ask whether the block matches a limit or protection you set, and consider using support tools if gambling feels hard to stop. |

| Withdrawal delayed | The delay may involve identity review, terms checks, bonus conditions or a complaint issue. | Save dates, balances, transaction references and messages. If the business is licensed, follow its complaint process before escalation. |

| Gambling feels difficult to control | Payment friction can become a sign that the issue is no longer only administrative. | Use protective tools rather than pushing through the barrier. Read the page on GAMSTOP, bank blocks and support options. |

Withdrawal friction: what to check without guessing

A delayed withdrawal does not prove bad faith on its own. It may be connected to identity checks, account ownership, payment-method rules, bonus terms or responsible-gambling reviews. But uncertainty is still a risk. A customer should know, before depositing, what documents may be requested, whether withdrawals can be held during checks, how bonus play affects cashout, and how a complaint is raised if the answer is unsatisfactory.

Be careful with phrases that promise “guaranteed withdrawals”, “no questions asked” or “instant approval” without clear conditions. Those phrases can create expectations that the written terms do not support. Written terms matter more than promotional wording. If the terms are hard to find, inconsistent or written in a way that ordinary users cannot understand, the safer decision is to step back.

Customer funds are another separate issue. A site can hold a customer balance, but that does not automatically mean the money is protected if the business fails. This is why the broader risk signals checklist includes customer-fund wording and complaint routes. A payment page should not pretend that a visible balance is the same as secure money.

What not to do

- Do not try to get around a credit-card restriction, e-wallet control, bank gambling block or self-exclusion tool.

- Do not assume that a site asking for documents only after a win is automatically unlawful; first compare the request with the written verification and withdrawal terms.

- Do not send identity documents through an insecure-looking channel or to a business whose licence status you cannot check.

- Do not keep depositing while a previous withdrawal is unresolved.

- Do not treat a foreign badge, fast-payment slogan or “no checks” message as a substitute for a Great Britain licence check.

Where this connects next

If the concern is whether the site is licensed for Great Britain, use the Gambling Commission register check guide. If the problem has already become a delayed payment, account closure or dispute, read what to do about a gambling complaint or disputed withdrawal. If a block or exclusion is active and gambling feels hard to control, focus on support and control tools rather than finding a way around the protection.

Created by the "Casino not on Gamstop" editorial team.